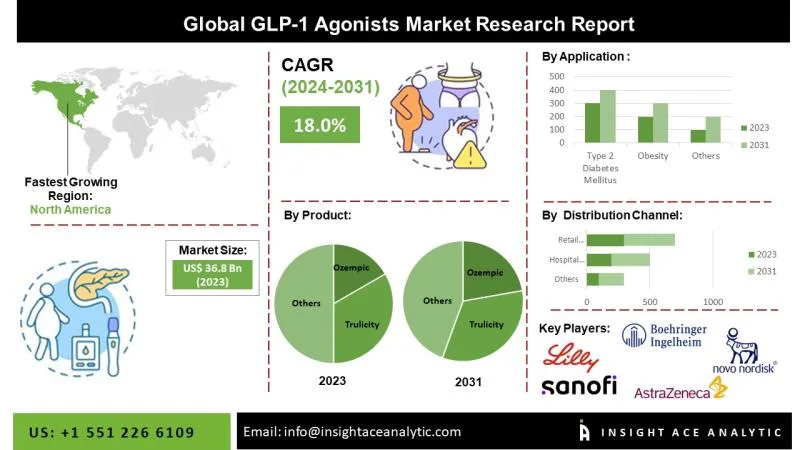

GLP-1 Agonist Market Surge: A Metabolic Shift Transforming Diabetes Treatment and Global Obesity Management

The GLP-1 Agonist Market is expanding at an unprecedented rate, fundamentally altering the global strategies for managing Type 2 Diabetes and treating obesity. This class of drugs, initially used for controlling blood sugar, has evolved into a significant therapeutic advancement for managing chronic weight issues, largely due to its effectiveness in regulating appetite and lowering cardiovascular risks. The soaring popularity of blockbuster drugs has triggered intense pharmaceutical competition, with the industry now focusing on creating next-generation dual and triple agonists that offer even more substantial metabolic benefits and overall health improvements. Health tracking apps like Shotlee can help monitor the effectiveness of these treatments.

Market Dynamics & Future

Innovation

Market growth is being fueled by the innovation in oral formulations and the development of multi-receptor agonists. These agonists target GIP/glucagon in addition to GLP-1 to achieve greater efficacy.

Consumer Shift

A significant shift is occurring as these drugs are increasingly seen not just as diabetes medication but as crucial lifestyle tools for weight loss and protecting cardiovascular health.

Distribution

Patient access and prescription fulfillment are mainly driven by retail pharmacies and the fast growth of telehealth platforms.

Future Outlook

The market's future will depend on addressing supply chain issues, broadening approved uses (like sleep apnea and kidney disease), and competing for insurance coverage.

Market Segmentation

By Drug Class:

- Semaglutide

- Dulaglutide

- Liraglutide

- Tirzepatide (Dual Agonist)

- Exenatide

- Lixisenatide

By Route of Administration:

- Parenteral (Subcutaneous Injection)

- Oral

By Application:

- Type 2 Diabetes Mellitus

- Obesity and Weight Management

- Cardiovascular Risk Reduction

- Others (NASH/MASH, CKD)

By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies & Telehealth

Region:

- North America

- U.S.

- Canada

- Mexico

- Europe

- U.K.

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- UAE

- Egypt

- South Africa

- Rest of Middle East and Africa

Competitive Landscape

Top Pharmaceutical Companies

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi S.A.

- AstraZeneca plc

- Boehringer Ingelheim

- Pfizer Inc. (Pipeline)

- Amgen Inc. (Pipeline)

- Roche (Pipeline)

- Viking Therapeutics

GLP-1 Agonist Regional Trends

The global market is divided geographically into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

North America (Dominant)

North America holds the largest market share due to a high prevalence of related diseases, strong insurance systems, and aggressive marketing of popular drugs like Ozempic, Wegovy, and Mounjaro. The U.S. is the main revenue source because of its higher drug prices.

Europe (Steady Growth)

Significant growth is expected in Europe, supported by its centralized healthcare and increasing regulatory approvals for using these drugs for weight management. The region prioritizes cost-effectiveness and extensive long-term safety information.

Precision tracking for your journey

Join thousands using Shotlee to accurately track GLP-1 medications and side effects.

📱 Get the Shotlee App

Track your GLP-1 medications, peptides, and health metrics on the go with our mobile app!

Asia-Pacific (Emerging Powerhouse)

Asia-Pacific is growing rapidly due to the increasing number of people with diabetes in China and India. This growth is driven by increased healthcare spending, urbanization, and the introduction of biosimilar drugs that make treatments more affordable.

Market Dynamics and Strategic Insights

The "Obesity Pivot"

The market has shifted from focusing solely on diabetes to a wider metabolic health perspective, with obesity now seen as a chronic condition needing long-term drug treatment.

Supply Chain Constrictions

High demand has exceeded global production capabilities, leading major companies to invest heavily in expanding their manufacturing facilities to address ongoing shortages.

Oral Formulation Race

While injectable drugs are currently dominant, the focus is shifting to oral delivery. Companies are working to develop highly effective pills to replace weekly injections, which could greatly improve patient compliance and market reach.

Insurance & Reimbursement

The evolving payer environment is a crucial factor, as employers and governments face pressure to cover anti-obesity medications (AOMs) despite their high cost, due to the potential for long-term savings by preventing cardiovascular complications.

Combination Therapies

The industry is moving beyond focusing on single hormones. The success of dual agonists (GLP-1/GIP) is encouraging research into "Triple G" agonists (GLP-1/GIP/Glucagon) to maximize weight loss results.

New Therapeutic Frontiers

Clinical trials are quickly broadening the use of GLP-1s beyond metabolic health, with promising results in treating addiction, Alzheimer's disease, and fatty liver disease (MASH).

Biosimilars Entry

As patents expire later in the decade, Asian manufacturers are preparing to launch affordable biosimilar versions, which will likely challenge the pricing power of current market leaders.