Peptide Therapeutics Market Size & Growth Analysis

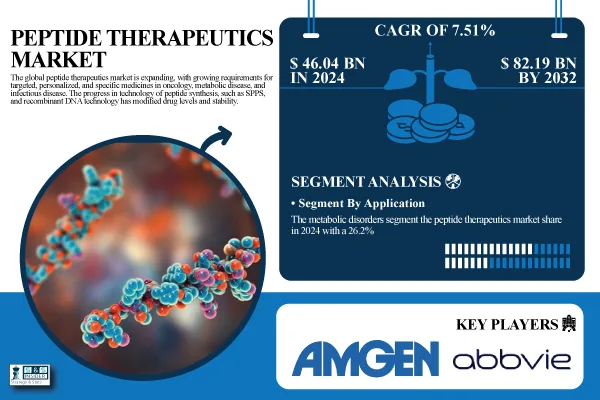

The global Peptide Therapeutics Market, valued at USD 46.04 billion in 2024, is projected to reach

USD 82.19 billion by 2032, exhibiting a CAGR of 7.51% from 2025 to 2032, according to SNS Insider. Market growth is being propelled by the increasing demand for customized and targeted medications for infectious diseases, metabolic disorders, and oncology.

U.S. Market Insights

The U.S. peptide therapeutics market, valued at USD 20.36 billion in 2024, is expected to reach

USD 35.71 billion by 2032, growing at a CAGR of 7.27% over the forecast period (2025-2032). The U.S. leads the North American market due to significant R&D investments, well-established regulatory frameworks, and rapid adoption of peptide treatments for chronic and metabolic conditions. Health tracking apps like

Shotlee can help monitor treatment effectiveness.

Key Drivers of Market Growth

Advancements in peptide synthesis and drug delivery technologies are boosting market expansion globally. These include:

- Solid-phase peptide synthesis (SPPS): Improvements have led to enhanced manufacturing efficiency, purity, and scalability.

- Recombinant DNA technology: Used in creating complex peptides.

- Liquid-phase peptide synthesis (LPPS): Another method to improve manufacturing.

Furthermore, advancements in delivery platforms, such as sustained-release formulations, nanoparticles, and

oral peptide formulations (like

semaglutide), are improving the usability and stability of peptide medications, thereby increasing their clinical use.

Challenges to Market Expansion

However, high production costs and complex manufacturing processes may restrain market growth. The synthesis and purification of peptide therapeutics are technically challenging and expensive. The majority of peptides are prepared using either Solid-Phase Peptide Synthesis (SPPS) or Recombinant DNA Technology, requiring complex steps, high-purity reagents, and expensive equipment.

Market Segmentation Highlights

By Therapeutic Area

In 2024, the metabolic disorders segment held a

26.2% share of the peptide therapeutics market, driven by the high prevalence of conditions like type 2

diabetes, obesity, and growth hormone deficiency globally. The pain segment is projected to experience the highest CAGR during the forecast period, fueled by rising occurrences of chronic pain disorders, increasing demand for non-opioid alternatives, and growing R&D investments in new peptide-based pain relievers.

By Therapeutics Type

The innovative segment dominated the market in 2024 due to the increasing need for targeted and high-activity treatment options. Pharmaceutical companies are focusing on advanced peptide engineering, delivery system design, and peptide hybrids.

By Type of Manufacturers

The in-house segment dominated with a

65.25% market share in 2024, as top biotech and pharmaceutical companies prefer control over the drug development process. The outsourced segment is expected to grow at the highest CAGR, driven by the increasing trend of small and mid-sized biotechnology companies partnering with contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs).

By Route of Administration

The parenteral route segment led the market in 2024 due to the poor oral bioavailability of most peptides, making injectable administration the most effective route. The other segment (including novel delivery pathways like transdermal, nasal, and buccal administration) is likely to grow at the highest CAGR due to technological advancements enhancing adherence and mitigating injectable limitations.

By Synthesis Technology

The recombinant DNA technology segment led the market in 2024 with a

64.3% market share, owing to its better performance in manufacturing long and sustained peptides with higher purity and biological activity. The liquid-phase peptide synthesis (LPPS) segment is expected to register the highest CAGR in the future due to its efficiency in synthesizing short to medium-length peptides with lower manufacturing costs.

Regional Analysis

North America dominated the market in 2024 with a

58.1% market share, driven by higher adoption of advanced clinical trial products, a developed pharmaceutical sector, increasing development of PCs in the region, and the presence of quality infrastructure. Asia Pacific is expected to grow significantly, driven by increasing healthcare expenditure, rising prevalence of chronic diseases, and growing pharmaceutical manufacturing facilities in countries like China, India, and South Korea.