Understanding GLP-1 Analogues: The Hormones Revolutionizing Metabolic Health

Glucagon-like peptide-1 (GLP-1) analogues mimic the GLP-1 hormone, naturally produced in the gut after eating. This hormone plays a crucial role in regulating blood sugar by stimulating insulin release, suppressing glucagon (which raises blood sugar), slowing gastric emptying, and promoting satiety in the brain. For patients with type 2 diabetes or obesity, these effects translate to better glycemic control and significant weight loss—often 10-20% of body weight in clinical trials.

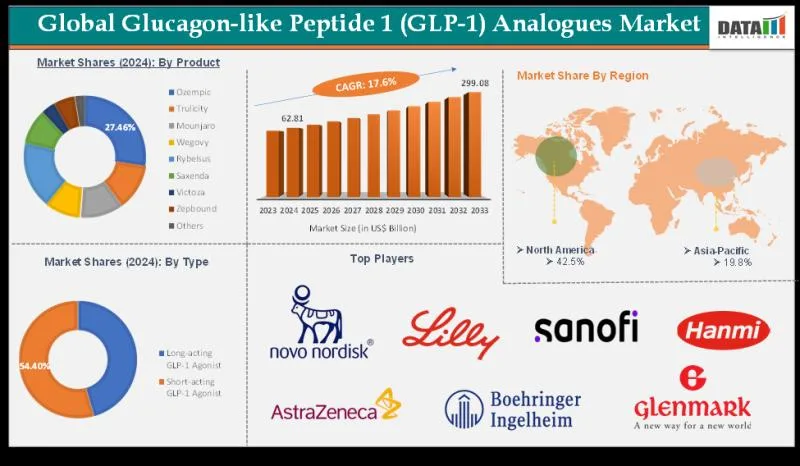

The market's explosive growth—from US$62.81 billion in 2024 to a projected US$299.08 billion by 2033 at a 17.6% CAGR—reflects surging demand. Rising global prevalence of diabetes (over 500 million adults) and obesity (1 in 8 people worldwide) are primary drivers, alongside expanded FDA approvals for weight management beyond diabetes.

Key GLP-1 Drugs: From Semaglutide to Tirzepatide

Semaglutide-based drugs like Ozempic (weekly injection for type 2 diabetes) and Wegovy (higher-dose for obesity) dominate market share. In the STEP trials, Wegovy users lost up to 15% body weight over 68 weeks, outperforming lifestyle interventions alone. Ozempic also reduces cardiovascular risk, as shown in the SUSTAIN-6 trial with a 26% drop in major events.

Mounjaro and Zepbound (tirzepatide), dual GLP-1/GIP agonists from Eli Lilly, are the fastest-growing. GIP enhances insulin secretion and fat metabolism. SURMOUNT-1 trial data revealed 22.5% average weight loss at the highest dose—superior to semaglutide. Trulicity (dulaglutide), Rybelsus (oral semaglutide), Saxenda (liraglutide), and Victoza round out options for varied needs.

Tirzepatide's dual action may explain its edge: GLP-1 curbs appetite, while GIP improves energy expenditure, per phase 3 studies.

Long-Acting vs. Short-Acting: Which Fits Your Lifestyle?

Long-acting GLP-1 agonists (e.g., Ozempic, Trulicity) lead with weekly dosing for convenience and steady control. Short-acting ones (e.g., some liraglutide formulations) target post-meal spikes but require daily use.

Administration Routes: Injections to Emerging Orals

Subcutaneous injections via user-friendly pens hold 80%+ market share for reliability. Oral options like Rybelsus are surging—taken daily on an empty stomach, it avoids needles but demands strict adherence. Future formulations promise even easier delivery.

Applications: Diabetes, Obesity, and Beyond

Type 2 diabetes claims the largest segment for glycemic control. Obesity is fastest-growing, with Wegovy and Zepbound approvals enabling chronic weight management. Emerging uses include cardiovascular protection (LEADER trial for liraglutide) and NASH (liver fat reduction in trials). Tools like Shotlee can help patients track symptoms, side effects, and nutrition alongside these therapies.

Precision tracking for your journey

Join thousands using Shotlee to accurately track GLP-1 medications and side effects.

📱 Get the Shotlee App

Track your GLP-1 medications, peptides, and health metrics on the go with our mobile app!

Market Segmentation: A Deeper Dive

- By Product: Ozempic/Wegovy lead; Mounjaro/Zepbound grow quickest due to superior efficacy.

- By Type: Long-acting dominates for adherence.

- By Route: Subcutaneous primary; oral expanding rapidly.

- By Distribution: Retail pharmacies top, with online surging for home delivery.

Regional Trends: North America Leads, Asia-Pacific Accelerates

North America holds the biggest share, thanks to high obesity rates (42% U.S. adults), FDA nods, and reimbursement. Asia-Pacific grows fastest—China and India's diabetes boom (140M+ cases) drives adoption, with guidelines emphasizing weight management.

Key Players and Innovations Fueling Growth

Eli Lilly (Mounjaro/Zepbound) and Novo Nordisk (Ozempic/Wegovy/Rybelsus) lead, with Sanofi, AstraZeneca, and Boehringer Ingelheim advancing combos and cardiovascular benefits. Recent moves include Eli Lilly's acquisition of dual-agonist tech and Novo Nordisk's peptide manufacturing buyout, signaling next-gen scalability.

Industry developments: Expanded U.S. access via insurance for Mounjaro/Zepbound; Novo Nordisk's digital adherence tools; Japan's focus on aging populations.

What Patients Need to Know: Dosing, Sides, and Success Tips

Start low (e.g., 0.25mg Ozempic weekly) to minimize nausea, the most common side effect (20-40% incidence, usually transient). Rare risks include pancreatitis or thyroid tumors—discuss family history with your doctor. Combine with diet/exercise: Protein-rich meals enhance satiety.

Monitor progress; apps like Shotlee track weight, glucose, and GI symptoms for personalized adjustments. Long-term data shows sustained benefits with adherence, but discontinuation often leads to regain—plan for maintenance.

Future Outlook: A $299 Billion Market by 2033

Projections hinge on oral innovations, dual/triple agonists (GLP-1/GIP/glucagon), and biosimilars lowering costs. Expanded indications like Alzheimer's (APP trials) could broaden reach. For patients, this means more options, better access, and evidence-based tools for metabolic health.

Conclusion: Navigating the GLP-1 Era

The GLP-1 market's boom underscores these drugs' transformative potential for diabetes and obesity. Ozempic, Wegovy, Mounjaro, and peers offer clinically proven results, but success demands medical guidance and lifestyle integration. Consult your provider to see if GLP-1s fit your goals—empowered choices lead to lasting health gains.