Overview of 2025 Approvals

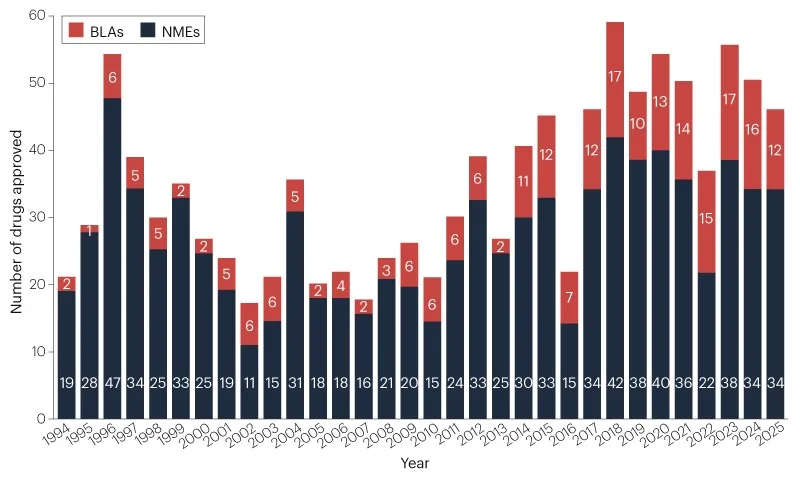

Pharmaceutical companies obtained clearance for 46 innovative therapeutic products from the FDA's Center for Drug Evaluation and Research (CDER) during 2025. This figure slightly reduces the five-year rolling average to 48 new medications annually, as illustrated in Figure 1 and Table 1. Nevertheless, it surpasses the long-term historical benchmark of 36 approvals per year dating back to 1993.

Therapeutic Areas in Focus

Oncology continues to be the predominant field for fresh drug endorsements. Out of the new CDER approvals, 16 (35%) targeted cancer treatments, exceeding the five-year rolling average of 29%. Cardiology followed with 5 (11%) clearances, and allergy alongside inflammatory conditions accounted for 4 (9%) each.

Emerging Modalities

Developers are progressing a wide range of treatment types, encompassing the initial adnectin-based biological medication, depicted in Figure 3.

This period also represented the largest year for kinase inhibitors, making up roughly one-third of the novel small-molecule approvals. Novartis's remibrutinib (Rhapsido) achieved the milestone of being the 100th kinase inhibitor to gain FDA endorsement, highlighting the ongoing growth of this drug category outside cancer care. "The field remains vibrant," noted Philip Cohen from the University of Dundee in an interview with Nature Reviews Drug Discovery.

The FDA has yet to disclose the classification of these approvals based on regulatory categories.

CBER Highlights

The Center for Biologics Evaluation and Research approved 8 significant new items, listed in Table 2, which includes the first gene therapy from a non-profit entity.

Sales Projections

An impending report from Boston Consulting Group indicates that the average maximum revenue for these fresh CDER and CBER approvals reaches approximately US$1.2 billion. The median stands at about $600 million.

Regulatory Environment

However, 2025 proved challenging for the FDA, characterized by significant personnel and policy shifts following President Donald Trump's appointment of Robert F. Kennedy Jr. to head the US Department of Health and Human Services. Over the initial nine months, over 18% of CDER and CBER staff departed through firings or resignations. CDER experienced five leadership changes throughout the year.

Despite these disruptions, the organization introduced fresh endorsement initiatives and routes. It initiated the FDA Commissioner's National Priority Voucher (CNPV) pilot program, designed to shorten review periods from the standard 10-12 months to just 2 months. Critics, including some FDA personnel and observers, argue that this initiative could introduce political influences into drug evaluations and compromise regulatory integrity. Additionally, the FDA suggested a viable mechanism pathway for cases where randomized studies are impractical, such as personalized n-of-1 treatments. It also outlined intentions to eliminate animal toxicity testing.

Further modifications are anticipated. Typically, the FDA mandates two key trials for complete approvals, but reports suggest a shift toward requiring only one trial as the standard.

Oncology Leadership

Cancer persists as the dominant area in the industry's development pipeline. Although oncology medications form the majority of new clearances, they contribute only two multi-billion-dollar drugs, each with annual revenue potential exceeding $2 billion as per Evaluate projections.

The highest-earning new approval is expected to be Merck & Co.'s subcutaneous version of pembrolizumab combined with berahyaluronidase alfa (Keytruda Qlex) for multiple solid tumors.

Pembrolizumab, an iconic PD1 inhibitor first cleared in 2014, activates immune cells against cancer cells. Berahyaluronidase alfa, an endoglycosidase enzyme, aids in antibody delivery by briefly degrading the subcutaneous extracellular matrix to enhance permeation and uptake. While hyaluronidase has served as a dispersing agent for years, this represents the initial endorsement for this modified protein form. Consequently, Merck's formulation qualifies as a new approval.

Pembrolizumab is projected to generate about $32 billion in 2025, positioning it as the leading cancer medication—and third overall in total sales. Analysts from Evaluate anticipate the subcutaneous variant to reach $9.3 billion at its peak.

Akeso Biopharma received clearance for its PD1 inhibitor penpulimab (Penpulimab), increasing the count of available PD1/PDL1 antibodies to 12.

This year also witnessed the endorsement of two fresh antibody-drug conjugates (ADCs), which combine tissue-specific antibodies with powerful cytotoxic agents. Daiichi Sankyo's TROP2-directed ADC datopotamab deruxtecan (Datroway) was approved for hormone receptor-positive, HER2-negative breast cancer after endocrine therapy and chemotherapy.

Evaluate predicts top earnings of $5.4 billion for this ADC, contingent on additional clearance in a larger non-small-cell lung cancer population. Gilead and Immunomedics's pioneering TROP2-targeted ADC sacituzumab govitecan (Trodelvy), initially granted accelerated approval in 2020, is poised to achieve $1.4 billion in 2025.

The FDA also cleared AbbVie's inaugural c-Met-targeted ADC, elisotuzumab vedotin (Emrelis). This microtubule-inhibitor carrying antibody is endorsed for non-squamous NSCLC with elevated c-Met protein levels.

Regeneron's linvoseltamab (Lynozyfic) introduces another bispecific T cell engager. It attaches to BCMA on B cells and CD3 on T cells to eliminate B cells in multiple myeloma treatment. This marks the third BCMA × CD3 bispecific available and the tenth bispecific T cell engager overall.

In the realm of kinase inhibitors, the FDA issued a unique dual-novel combination clearance for two formerly investigational compounds. Verastem's avutometinib plus defactinib (Avmapki Fakzynja Co-Pack) pairs a MEK inhibitor with a FAK inhibitor to address KRAS-mutated recurrent low-grade serous ovarian cancer.

Defactinib represents the first FAK inhibitor to receive approval. Several MEK inhibitors have previously been cleared. The FDA considers these two innovative kinase inhibitors as one new drug approval.

"Individuals should embrace novel-novel combinations more readily," stated Verastem's CSO Jonathon Pachter in Nature Reviews Drug Discovery.

Jazz Pharmaceuticals' pioneering activator of mitochondrial caseinolytic protease P (ClpP) dordaviprone (Modeyso) earned accelerated approval for diffuse midline gliomas with H3 K27M mutations in patients showing progression after prior treatments. ClpP degrades mitochondrial proteins, and its stimulation is thought to trigger the integrated stress response, cell death, and the release of substances that counteract the growth effects of H3 K27M mutations.

Non-Oncology Breakthroughs

Non-cancer CDER endorsements included two potential mega-blockbuster prospects with novel mechanisms for emerging indications.

Insmed's brensocatib (Brinsupri) stands as the inaugural DPP1 inhibitor on the market, targeting bronchiectasis and illustrating the promise of neutrophil-focused medications in lung inflammatory conditions.

Bronchiectasis is a persistent lung ailment leading to excessive mucus, chronic coughing, and airway enlargement. It impacts 350,000 to 500,000 individuals in the USA, with previous treatments limited to physical therapy for mucus removal and antibiotics for infections. The condition links to hyperactive neutrophils, immune cells that secrete antimicrobial peptides known as neutrophil serine proteases (NSPs) to combat pathogens. Brensocatib, a DPP1 inhibitor, curbs NSP production, neutralizing these inflammatory enzymes without affecting other neutrophil functions.

"This is an encouraging era—to inform patients about upcoming options that could truly assist them," remarked Doreen Addrizzo-Harris, a pulmonologist at NYU Langone Health involved in brensocatib trials, to Nature Reviews Drug Discovery.

Analysts project peak revenue of $6.3 billion for the medication, assuming extensions to other neutrophil-related disorders. However, in December, the firm halted development in chronic rhinosinusitis due to insufficient reduction in nasal swelling.

Vertex's Na1.8 sodium channel blocker suzetrigine (Journavx) offers a vital opioid-free alternative for acute pain relief. Since the 2000s, researchers have pursued Na channel inhibition after discovering that mutations in Na1.7 channels cause ongoing pain issues, while loss-of-function variants block pain sensation. Na1.7 inhibitors have underperformed clinically, yet Vertex advanced with the analogous Na1.8 channel.

"This represents the first medication engineered solely for pain management," explained Paul Negulescu, senior vice president of research at Vertex, in Nature Reviews Drug Discovery. "Suzetrigine marks the start, not the finish, of this novel drug category."

Analysts foresee peak sales of $3.7 billion, driven by the demand for non-addictive analgesics and potential in chronic pain. Challenges persist, as approval relied on non-inferiority to acetaminophen-opioid mixes for post-surgical acute pain, with uncertainty in other acute scenarios. It also carries a higher cost than generic options. Effectiveness in chronic conditions remains unproven, with ongoing Phase III trials in diabetic peripheral neuropathy, though it failed in lumbosacral radiculopathy.

Later in the year, Vertex abandoned development of the succeeding Na1.8 inhibitor VX-993 for acute pain after Phase II setbacks.

Additional First-in-Class Medications

Other pioneering agents expand the pharmacological arsenal, though with modest sales outlook.

For instance, GSK's gepotidacin (Blujepa) delivers a necessary fresh oral antibiotic choice. Similar to quinolone antibiotics dating back to the 1960s, gepotidacin targets bacterial type IIA topoisomerases. Yet, it employs a distinct framework and interacts with the enzyme at a different location, earning its first-in-class status. The FDA initially cleared it in May for uncomplicated urinary tract infections in females and children aged 12 and up. By December, it gained approval for gonorrhea.

Innoviva Specialty Therapeutics' zoliflodacin (Nozolvence), another unique bacterial type II topoisomerase inhibitor, received FDA clearance for gonorrhea. Phase III studies for zoliflodacin were sponsored and conducted by the Global Antibiotic Research & Development Partnership (GARDP), a public non-profit aiming for global availability. Innoviva acquired it through the purchase of Entasis Therapeutics, a AstraZeneca spin-off.

Precision tracking for your journey

Join thousands using Shotlee to accurately track GLP-1 medications and side effects.

📱 Get the Shotlee App

Track your GLP-1 medications, peptides, and health metrics on the go with our mobile app!

Kinase inhibitors are extending into inflammatory and immune disorders, primarily via BTK-acting compounds. Originally approved for blood cancers by eliminating malignant B cells, they also modulate immune cell behavior. This year, Sanofi secured the initial clearance for rilzabrutinib (Wayrilz) in immune thrombocytopenia, an immune blood condition. Novartis obtained approval for remibrutinib (Rhapsido) in chronic spontaneous urticaria, or persistent hives.

Analysts predict top earnings of $2.1 billion for remibrutinib, which is under development for multiple sclerosis, myasthenia gravis, hidradenitis suppurativa, and food allergies. They estimate $900 million peak sales for Sanofi's rilzabrutinib.

In contrast, the agency denied Sanofi's BTK inhibitor tolebrutinib for multiple sclerosis.

Boehringer Ingelheim's nerandomilast (Jascayd) emerged as the first PDE4 inhibitor for idiopathic pulmonary fibrosis (IPF).

PDE4 inhibitors with anti-inflammatory and immunomodulatory effects have been cleared for conditions like chronic obstructive pulmonary disease and psoriasis. Boehringer now adds IPF approval, a progressive fatal lung disorder affecting up to 3.6 million globally. Nerandomilast selectively targets the PDE4B subtype to reduce fibrosis and lung inflammation.

This is the first new medication for IPF in over a decade, following nintedanib (Ofev) from Boehringer, a multikinase inhibitor cleared in 2014, and pirfenidone (Esbriet), now by Legacy Pharma.

LIB Therapeutics achieved the first approval for an adnectin-based treatment with PCSK9 inhibitor lerodalcibep (Lerochol).

Adnectins are biologics constructed from fibronectin type III domains, proteins that support cell interactions and can attach to various ligands. For years, scientists have proposed adnectins as antibody alternatives, providing precise targeting for extracellular or cell-surface molecules with compact, stable designs compared to monoclonal antibodies.

LIB utilized this approach to create the newest PCSK9 blocker, a validated target for cholesterol reduction. PCSK9 antibodies have been available for a decade, but adoption lags due to high costs and injection inconvenience versus generic pills. LIB anticipates lerodalcibep's advantages—a self-administered monthly subcutaneous dose with extended stability at room temperature.

Oral small-molecule PCSK9 inhibitors may arrive soon. Merck & Co. plans to submit enlicitide, a daily pill, for approval in April. Granted a CNPV, it could undergo rapid review. Upon clearance, the firm intends to offer it affordably for US patients.

Advances in Rare Diseases

Individuals with hereditary angioedema (HAE) accessed three new medications.

HAE is a genetic swelling condition steming from C1 inhibitor deficiencies or malfunctions, a regulator of serine proteases. This leads to heightened complement protease, plasma kallikrein, and coagulation protease activity (factor XIa, XIIa, XIIf).

CSL Behring's prophylactic antibody garadacimab (Andembry) targets activated factor XII to avert episodes. Ionis's antisense oligonucleotide donidalorsen (Dawnzera) addresses prekallikrein to prevent attacks. Kalvista's small-molecule plasma kallikrein inhibitor sebetralstat (Ekterly) treats acute flares.

These enter a competitive HAE landscape with existing preventive and acute therapies affecting different pathway points.

Patients at risk for progression in primary immunoglobulin A nephropathy (IgAN) received two novel treatments. IgAN, an immune kidney disorder, involves IgA-immune complex buildup causing gradual renal function loss and potential failure. Otsuka's sibeprenlimab (Voyxact), a pioneering APRIL-targeted antibody, curbs IgA production to lessen proteinuria. Novartis's atrasentan (Vanrafia), an endothelin receptor blocker, reduces glomerular pressure and kidney inflammation.

Vera Therapeutics' atacicept, a fusion protein inhibiting BLyS and APRIL, awaits FDA decision for IgAN in 2026.

Gene Therapy Progress

CBER continues to accumulate gene therapy clearances. This encompasses the initial non-profit approval, Fondazione Telethon ETS's for etuvetidigene autotemcel (Waskyra) in Wiskott-Aldrich syndrome (WAS).

WAS, a genetic disorder from WAS gene mutations causing faulty platelets, is treated by etuvetidigene autotemcel, an ex vivo gene therapy using lentiviral vectors to insert the WAS sequence into patient hematopoietic stem cells, restoring platelet function. Originating from a 2010 collaboration between Fondazione Telethon, San Raffaele Telethon Institute for Gene Therapy, and GSK, it demonstrated lasting effectiveness. After GSK's gene therapy commercialization struggles, it transferred to Orchard Therapeutics, then to Fondazione Telethon in 2022.

Fondazione Telethon will partner with Orphan Therapeutics Accelerator, a non-profit biotech, for US access. They anticipate treating under 10 US patients yearly, with ongoing pricing talks. The gene therapy field monitors this non-profit framework.

"As a researcher, I underestimated the effort in submitting and sustaining a market drug," shared Alessandro Aiuti, deputy clinical research director at San Raffaele Telethon Institute for Gene Therapy, who aided approval, with Nature Reviews Drug Discovery.

The FDA also cleared Abeona Therapeutics' prademagene zamikeracel (Zevaskyn), the first cell-sheet gene therapy for severe skin disorders. It involves biopsied patient skin cells transduced to express type VII collagen, grown into card-sized sheets for wound grafts. Approved for recessive dystrophic epidermolysis bullosa (DEB), a genetic skin fragility from type VII collagen gene mutations.

In 2023, Krystal Biotech's beremagene geperpavec (Vyjuvek), a topical redosable type VII collagen gene therapy, was approved for DEB wound healing.

Precigen's zopapogene imadenovec (Papzimeos) is the inaugural immunotherapy for recurrent respiratory papillomatosis (RRP), an HPV-caused airway growth disorder. It uses a non-replicating gorilla adenovirus vector with HPV 6 and 11 genes to elicit T cell responses against HPV, clearing growths.

CBER granted full clearance to two new COVID-19 vaccines. Moderna's mNexspike, an advanced mRNA vaccine, employs one-fifth the mRNA of Spikevax and encodes partial spike protein. Analysts project over $3.2 billion in sales.

Policy Changes and Rejections

In another shift, the FDA began issuing partially censored complete response letters for denied drugs. By December 31, it listed 43 rejections in 2025, covering new drugs (Table 3), supplements, generics, and biosimilars for CDER or CBER.

Scholar Rock faced a complete response letter for apitegromab, an anti-promyostatin antibody for spinal muscular atrophy, due to third-party manufacturing issues. They plan resubmission after fixes.

Regeneron received a second denial for odronextamab, a CD20 × CD3 bispecific for follicular lymphoma, partly from the same manufacturing problems.

Stealth Bio got a May rejection for elampretide, a mitochondrial cardiolipin binder for Barth syndrome, lacking efficacy evidence for full or accelerated approval. They resubmitted with a new endpoint and gained September approval.

The agency also rebuffed Replimune's vusolimogene oderparepvec, potentially the first new oncolytic virus since Amgen's talimogene laherparepvec (Imlygic) in 2015. Trials with nivolumab in melanoma showed higher response rates than controls, but population variability complicates interpretation, and effects weren't separated from nivolumab. They resubmitted, with a decision pending in April.

Upcoming Approvals

Several innovative medications may receive initial clearances next year (Table 4).

Arvinas and Pfizer's oestrogen receptor-targeted vepdegestrant could be the first targeted-protein degrader approved. While selective oestrogen receptor degraders exist, vepdegestrant is a two-armed PROTAC linking the receptor to proteasomal components for degradation. It has struggled to stand out from other SERDs, and partners seek to license it.

If cleared, it would affirm targeted degraders, potentially enabling drugging of intractable targets with molecular glue variants.

Denali Therapeutics anticipates approval for tividenofusp alfa, an enzyme replacement for Hunter syndrome. Takeda's idursulfase (Elaprase), an IDS enzyme therapy since 2006, doesn't penetrate the brain well for neurological issues. Tividenofusp alfa fuses IDS to an Fc fragment binding transferrin receptors for CNS entry.

Regenxbio may secure clearance for clemidsogene lanparvovec, a CNS-injected gene therapy for Hunter syndrome.